Why you got auto-assigned to a default fund

In June 2025 the Ministry of Finance turned on a rule that quietly affects every new Israeli employee at a company with 50 or more workers: if you do not actively choose a pension fund within 60 days, you get allocated to one of four designated default funds based on the last digit of your Israeli ID number. This chapter explains the mechanism, names the four funds, and answers the question every reader has by now: is the default fund the BEST fund, or just a CONVENIENT one?

The four default funds, 2021 through 2028

Every three to four years, the Capital Markets Authority runs a tender (מכרז קרנות ברירת מחדל) and selects the funds that will serve as defaults for the next period. The current designation runs from November 1, 2021 through October 31, 2028. The four funds:

| Fund | Hebrew name | Operator type |

|---|---|---|

| Altshuler Shaham Pension | אלטשולר שחם גמל ופנסיה | Investment house |

| Meitav | מיטב בית השקעות | Investment house |

| Mor Gemel ve-Pension | מור קופות גמל | Investment house |

| Infiniti | אינפיניטי ניהול השתלמות וגמל | Investment house |

Notice what is NOT on this list: the large traditional insurance houses (Migdal, Menorah Mivtachim, Harel, Phoenix, Clal). They run pension funds, but they are not part of the current default tender. That is a regulatory decision by the Capital Markets Authority, not a quality judgment.

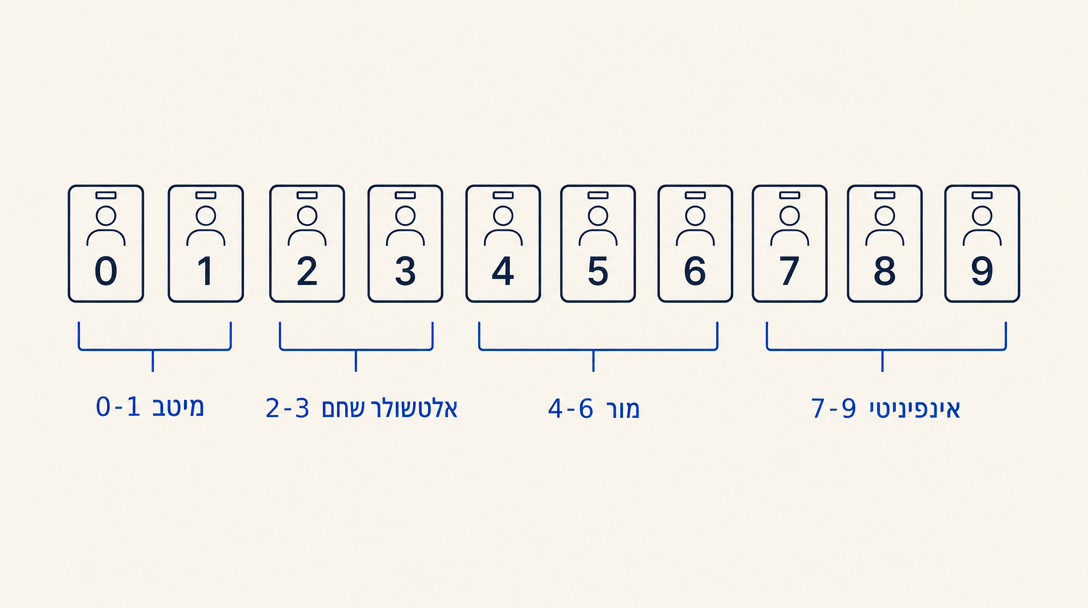

Auto-allocation: how you get assigned

Since June 2025, if you join a company with 50+ employees and do not pick a fund within 60 days, you are allocated by your ID check-digit (the last digit of your תעודת זהות):

| Last digit of your ID | Allocated to |

|---|---|

| 0 or 1 | Meitav |

| 2 or 3 | Altshuler Shaham |

| 4, 5, or 6 | Mor |

| 7, 8, or 9 | Infiniti |

If your employer has fewer than 50 employees, the default-allocation rule does not apply automatically. The employer must still enroll you in a pension fund, but they may pick any one of them as the workplace default.

The regulated fee cap during the default period

In exchange for being designated, the four default funds agree to a regulated fee ceiling that lasts the full default period, applicable to anyone who joins one of these four funds (whether through auto-allocation or by active choice):

"שיעור דמי הניהול המקסימליים של ארבע קרנות הפנסיה הנבחרות: 0.22% מהצבירה, 1% מההפקדות."

Translation: maximum management fees for the four selected pension funds are 0.22 percent of accumulated savings and 1 percent of new deposits. That is the lowest regulated fee tier in the market. By comparison, the regulatory MAXIMUM for any pension fund is 0.5 percent on accumulation and 6 percent on deposits; in practice, non-default funds with no negotiated discount commonly charge 0.3 to 0.5 percent on accumulation and 1.5 to 4 percent on deposits, with collectively-bargained workplace agreements often securing lower rates. The point is that fees vary widely outside the four designated funds, and grandfathered fee schedules from older contracts may persist even if a fund's current rate card looks competitive.

So is the default fund the BEST fund?

No. It is the fund with the regulated-cap fees. Fees are one of two axes that determine your 40-year outcome; returns are the other. The default-fund mechanism guarantees the first axis (low fees) but not the second (high returns).

In the 5-year cumulative returns published by the official פנסיה נט portal at the end of 2025, the top three positions in the age-based tracks (the relevant tracks for most Israelis) were taken by Phoenix, Clal, and Meitav. Of those three, only Meitav is a default fund. Phoenix and Clal are not in the current default tender at all.

Meaning: an Israeli who got auto-allocated to Meitav is in a fund with both regulated-cap fees AND a top-3 long-term return record. An Israeli auto-allocated to one of the other three default funds got the fees but not (necessarily) the returns.

The most common mistake in Chapter 3: assuming the default fund's regulated fees compensate for any return difference. They often do (the fee gap can be substantial and compounds over decades), but a meaningfully lower return on the same time window can wipe out the fee advantage. The right way to check is to compare your fund's 5-year cumulative return to the same-track cohort leaders, which is exactly what Chapter 4 walks through.

For Israeli employees who want to verify which fund their employer enrolled them in, and how the auto-allocation rule interacts with mandatory contributions from Bituach Leumi (such as the old-age pension layer קצבת זקנה), the israeli-bituach-leumi skill is at https://agentskills.co.il/skills/israeli-bituach-leumi.

Want to keep reading?

Sign in to unlock the rest of the course and track your progress.