Self-employed pension (mandatory since 2017)

If you are an osek patur or osek murshe, you are required by law to contribute to a pension fund. The law is called חוק פנסיה חובה לעצמאים, in force since January 2017. The penalty for non-compliance is approximately ₪500 per year, which is so low that many self-employed people just pay the fine and skip the contribution. They are leaving an order of magnitude more in tax benefit on the table than the fine costs. This chapter explains why, with the 2026 numbers.

The 2026 contribution bands

Self-employed pension contributions are calculated on your annual taxable income (הכנסה חייבת), in two bands tied to the average wage (₪13,769/month × 12 = ₪165,228/year):

| Annual income band | Mandatory contribution rate | What it covers |

|---|---|---|

| Income up to ₪82,614 (half of average wage × 12) | 4.45% | The minimum to satisfy the mandate |

| Income from ₪82,615 to ₪165,228 (between half and full average wage) | 12.55% | Mandate on the next slice |

| Income above ₪165,228 | Voluntary (but tax-advantaged) | See tax benefits below |

A self-employed person earning ₪120,000/year falls partly in the low band (4.45% on the first ₪82,614 = ₪3,676) and partly in the high band (12.55% on the next ₪37,386 = ₪4,692), for a total mandatory contribution of approximately ₪8,368/year. Skipping it costs ₪500 in fines. Doing it right unlocks the tax benefit ladder described next.

The 2026 tax benefit ladder

This is what self-employed people miss when they "just pay the fine." The benefit comes through two parallel channels, both indexed to your annual income up to the ₪232,800 cap.

-

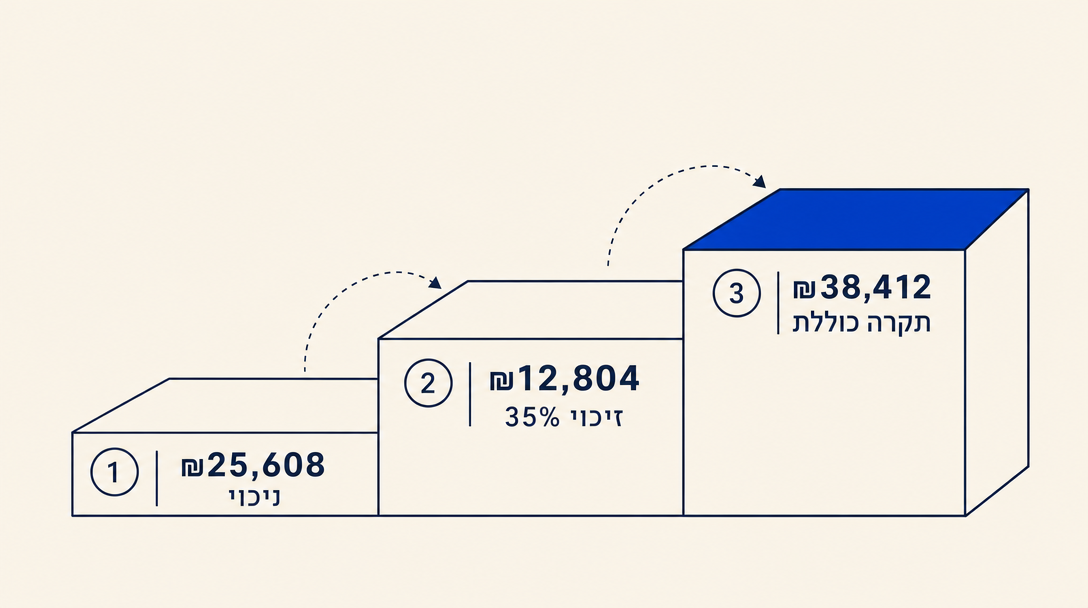

Deduction channel (ניכוי), up to 11 percent of income, capped at ₪25,608/year. A self-employed person earning ₪232,800 hits the deduction cap by contributing ₪25,608 (11 percent of income). This portion comes off your taxable income; at a 35 percent marginal rate it is worth roughly ₪8,963 in tax saved.

-

Credit channel (זיכוי), an additional 5.5 percent of income, capped at ₪12,804/year, earning a 35 percent credit. On top of the deduction, you can contribute another 5.5 percent of income (up to ₪12,804 at the cap), and the tax authority returns 35 percent of that contribution as a credit, regardless of your marginal rate. At the cap that credit is roughly ₪4,481.

-

Combined tax-advantaged cap: 16.5 percent of income, up to ₪38,412/year. The two channels apply to two stacked slices of the SAME annual income (the first 11 percent and the next 5.5 percent). They do not double-up on the same money. At the ₪232,800 income cap, the maximum tax-advantaged contribution is ₪25,608 + ₪12,804 = ₪38,412 per year, and the combined tax savings are approximately ₪13,400 (₪8,963 + ₪4,481).

For incomes below ₪232,800, the caps scale down proportionally: a self-employed person earning ₪120,000 can deduct up to 11 percent (₪13,200) and contribute another 5.5 percent (₪6,600) into the credit channel, total ₪19,800 tax-advantaged.

The fine for non-compliance is ₪500. The forgone tax benefit can be ₪10,000+. The math does not require a calculator.

Worked example: ₪200k/year freelancer

A freelancer with ₪200,000 in taxable income in 2026. The numbers below are approximations to illustrate the structure; your accountant should compute your exact figures, since the deduction and credit channels can interact with other deductions on your return.

| Strategy | Contribution | Pension savings accrued | Approximate net tax effect |

|---|---|---|---|

| Pay the fine, contribute nothing | ₪0 | ₪0 | ₪0, plus a ₪500 fine |

| Mandatory minimum only | About ₪18,400 (4.45% on first band + 12.55% on the next ₪117,386) | About ₪18,400 in fund | Roughly ₪6,400 reduction in tax owed |

| Optimized for full tax channels | Up to ₪33,000 (16.5% of ₪200,000 income) | About ₪33,000 in fund | Roughly ₪11,500 reduction in tax owed |

The third path requires the freelancer to put roughly ₪14,600 of additional cash into the pension fund (beyond the mandatory minimum). In exchange, the fund balance grows by ₪14,600 of locked-in retirement savings AND the additional tax reduction is roughly ₪5,100 vs the minimum-only path. This is tax efficiency, not investment return: the additional ₪14,600 is your own money, locked in the fund until age 60+, subject to fees and market risk. Treat it as "I am moving money I would have paid in tax into a long-term savings account that holds it for me" rather than as a return on capital.

Pairing strategy: keren pensia + keren hishtalmut

The full self-employed tax stack is not just the pension fund. The next layer is קרן השתלמות (training fund), a separate provident-fund product with its own deduction cap (covered in detail by the israeli-pension-advisor skill and by the israeli-freelancer-year course's chapter 4). The combined annual ceiling across pension + keren hishtalmut is substantial for a high-earning self-employed person; most freelancers structure their year around hitting both ceilings rather than just the pension cap. Your accountant should run your specific numbers.

The most common mistake in Chapter 5: paying the fine to skip the mandate. The fix: open your annual tax planning conversation with your accountant by asking "how do I max out the pension + keren hishtalmut tax stack this year?" and adjust monthly cash flow to hit it.

For ongoing detailed questions about which contribution channel fits which scenario (and especially for the keren hishtalmut layer), the israeli-pension-advisor skill is the right tool. The course gets you to the planning conversation; the skill walks you through the line-item math.

Want to keep reading?

Sign in to unlock the rest of the course and track your progress.