The two-question decision tree

Every pension question worth asking reduces to two: do you need a fund right now, and who inherits if something happens to you tomorrow? Most Israelis answer Q1 correctly (employer enrolls them automatically) and then never think about Q2 again. That asymmetry is the single largest source of preventable financial mistakes in Israeli pension.

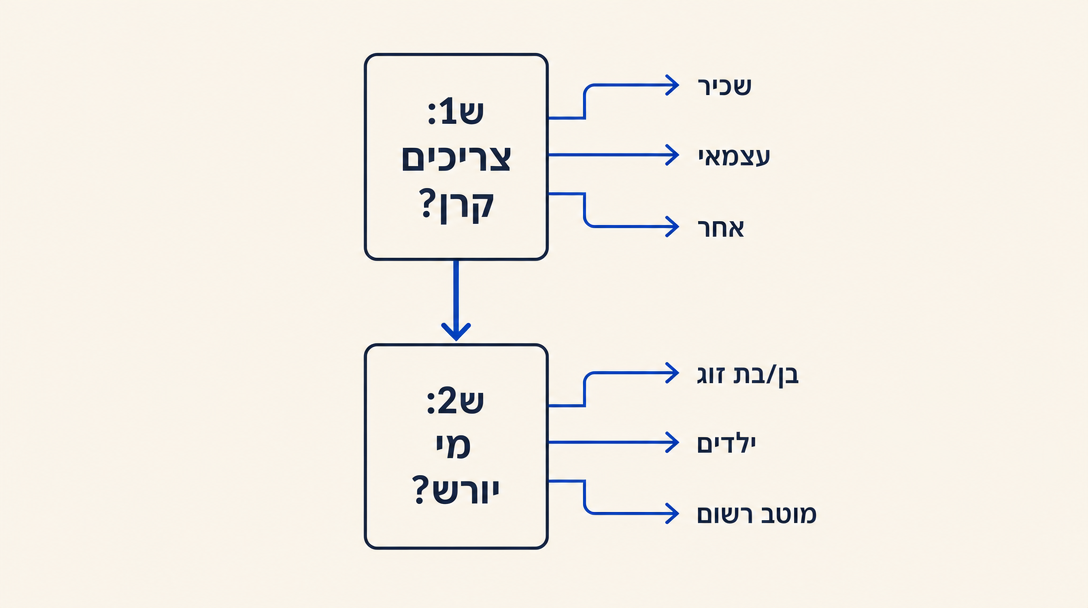

Q1: Do you need a pension fund right now?

Israeli pension is mandatory in three different ways for three different audiences. The decision tree:

-

Salaried employee with prior pension coverage in the last 12 months. Mandatory from day 1 on the new job. Your employer must deduct your 6 percent and add 6.5 percent + 8.33 percent severance starting with the first payslip.

-

Salaried employee with NO prior pension coverage (first job, or back from a long break). Mandatory from month 7. The employer must enroll you no later than the seventh full month of employment, retroactive to month 1 of the relevant tax year. If your employer "forgets," they owe you back-contributions plus statutory interest, and the Ministry of Labor enforces it.

-

Self-employed (osek patur or osek murshe). Mandatory since the 2017 חוק פנסיה חובה לעצמאים (Mandatory Pension for the Self-Employed Law). You enroll yourself directly with a fund. Penalty for non-compliance: roughly ₪500 per year, which is so low that many self-employed people pay the fine and skip the contribution. Chapter 5 explains why that math is wrong (you are leaving thousands of shekels of tax benefit on the table).

-

Student / part-time at one job / contractor invoicing through a personal account. It depends on your status: if you are W2 (שכיר) at any percentage, you fall under the employee mandate. If you invoice as an עוסק, the self-employed mandate applies. There is no exempt category for "I only work a few hours."

If you are in any of the first three categories and you are not currently contributing, you have a problem to fix this week, not next year.

Q2: Who inherits if something happens to you tomorrow?

This is where many Israelis make a quiet, expensive mistake. The pension fund's survivor rules are NOT set by your will. They are set by the fund's regulation (תקנון הקרן), and the eligibility definitions of "spouse" and "orphan" are referenced from the Bituach Leumi statutory definitions.

Eligible survivors, in order:

-

Spouse (אלמן/אלמנה or ידוע/ידועה בציבור). Common-law partners count, including same-sex partners. A surviving spouse receives the pension fund's survivor pension regardless of their own income. (Note: do not confuse this with Bituach Leumi's separate survivor benefit (קצבת שאירים from ביטוח לאומי), which DOES have an income test. Pension fund survivor pension and Bituach Leumi survivor benefit are two different programs.)

-

Orphan (יתום). Any child of the deceased under age 21. They receive a monthly pension until they turn 21. Some funds extend coverage during mandatory military or national service, and exception rules exist for orphans in higher education.

-

Disabled adult orphan or dependent parent. Specific eligibility rules, mostly tied to financial dependence on the deceased. A disabled adult orphan (orphan with permanent disability) may receive lifetime survivor pension under separate provisions of the fund's תקנון.

-

If none of the above exist: the accumulated savings are paid out as a lump sum to your designated beneficiaries (the form you fill in at the fund). If you never filled in that form, the money goes to your legal heirs via court order (צו ירושה or צו קיום צוואה). The court order process commonly takes months and incurs lawyer/court fees that vary widely depending on contestation and complexity; budget for it before the need arises.

Two scenarios that play out very differently

Scenario A: Married, 2 kids, no will, beneficiary form never updated. You die. Spouse gets monthly pension for life. Both kids get monthly orphan pension until 21. Smooth, regulated, fast. The "no will" detail does not matter here because survivor pension is regulated, not testamentary.

Scenario B: Divorced, no children, beneficiary form still names ex-spouse from 8 years ago. You die. The fund pays the lump sum to the named beneficiary (your ex). Your current partner (not registered as common-law) gets nothing. Your parents get nothing. This is the most common avoidable mistake in the Israeli pension system, and it is fixed by 5 minutes on your fund's website.

The most common mistake in Q2: never updating the beneficiary form after marriage, divorce, the birth of a child, or the death of a parent. Open your fund's portal this week. Find the form called הסכם מינוי מוטבים or כתב הצהרת מוטבים. Update it.

For more nuanced cases (the spouse income test, common-law without registration, blended families), the israeli-pension-advisor skill walks through the specific rules in conversation. The course gives you the framework; the skill answers the specific question.

Want to keep reading?

Sign in to unlock the rest of the course and track your progress.