How to think about the freelancer year

Most freelancers know the deadlines exist. They have a calendar app reminder for the 15th of every month, they file the Doch Maam, they pay the mkdamot, they panic in April. That's not a year. That's a treadmill.

A real freelancer year has four phases. Each phase has a posture: what you're doing, what you're watching, what you're deciding. Once you see the year as four phases instead of twelve identical months, the strategic decisions become obvious.

The four-quarter model

Q1 (January through March): orient and react. You're closing the previous year. Annual VAT return is due January 31. You're gathering documentation for the April 30 income tax return. Your mkdamot for the current year are still set from the previous year's income, and they will be wrong if your revenue changed. You're not making strategic decisions yet because you don't have enough data on the current year. What you're doing: closing the books, filing, and reading what the previous year is telling you.

Q2 (April through June): commit and adjust. You've filed your annual return. You know what you actually paid in tax last year. Now your current year is taking shape: you can see Q1 actuals and start projecting the full year. This is when most freelancers should consider their first tikun mkdamot (mkdamot adjustment), your current run-rate is now visible. You're also locking in big-ticket structural decisions: stay osek patur or upgrade to osek murshe? Switch VAT cadence?

Q3 (July through September): operate and watch. This is the calm quarter. You're executing on the strategy set in Q2. You're watching for income trajectory shifts that would justify a second tikun mkdamot. You're tracking expenses that you might pull forward or defer in Q4. The osek patur threshold (₪122,833 in 2026 per the Tax Authority) is starting to come into focus for borderline freelancers, if you're tracking to cross it, this is when you start preparing the switch.

Q4 (October through December): steer. This is where you make the biggest tax-bill-shaping decisions of the year. Final expense timing. Final keren hishtalmut contribution. Section 46 charity donations have a December 31 deadline. The "issue invoice on Dec 31 vs Jan 1" question. Most freelancers blow Q4 because they treat it like Q3, and discover in April that they paid more tax than they had to.

The whole year in one table:

| Quarter | Phase | Posture | What you decide |

|---|---|---|---|

| Q1 | orient and react | closing | nothing strategic yet |

| Q2 | commit and adjust | committing | osek status, VAT cadence, tikun mkdamot |

| Q3 | operate and watch | maintaining | expense planning, threshold tracking |

| Q4 | steer | steering | timing, contributions, charity |

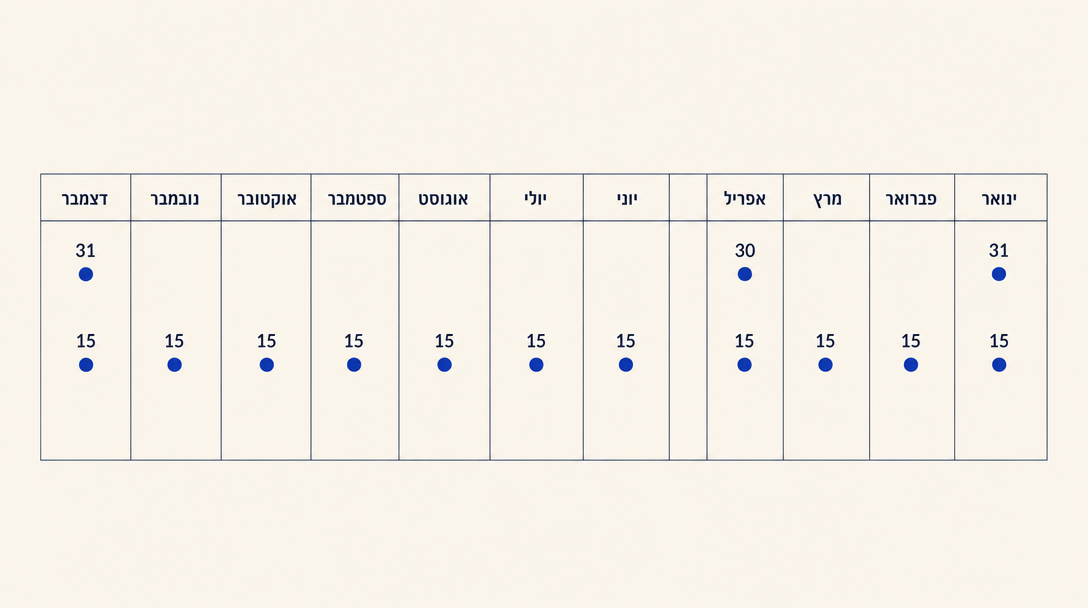

The 12 fixed deadlines

These are the dates you cannot move. They're set by the Tax Authority and Bituach Leumi. The exact date for some shifts based on whether you're a monthly or bi-monthly VAT filer (chapter 2 explains how to decide), but the structure is the same.

| Month | Deadline | Who it applies to |

|---|---|---|

| January 15 | Bituach Leumi atzmai payment (December prior year) | All atzmaim |

| January 15 | Income tax mkdamot (December prior year) | Mkdamot payers |

| January 15 | Doch Maam for December (monthly filers) OR Nov-Dec (bi-monthly) | Osek murshe |

| January 31 | Final annual VAT return | Osek murshe |

| Every 15 of month (or bi-monthly) | Doch Maam | Osek murshe |

| Every 15 of month | Bituach Leumi atzmai | All atzmaim |

| Every 15 of month | Income tax mkdamot | Mkdamot payers |

| April 30 | Form 1301 annual income tax return | All atzmaim (extensions available) |

| April 30 | Final reconciliation of prior-year mkdamot | All atzmaim |

| Throughout year | Eilat-zone exemption renewals if applicable | Eilat-resident freelancers |

| December 31 | Section 46 charity donations cutoff | All taxpayers |

| December 31 | Keren hishtalmut atzmai contribution cutoff for current tax year | All atzmaim |

The Form 1301 April 30 deadline is the most-missed date in the calendar because extensions are available "with proper documentation" but freelancers assume they're automatic. They're not. Plan to file by April 30 by default; treat the extension as a fallback.

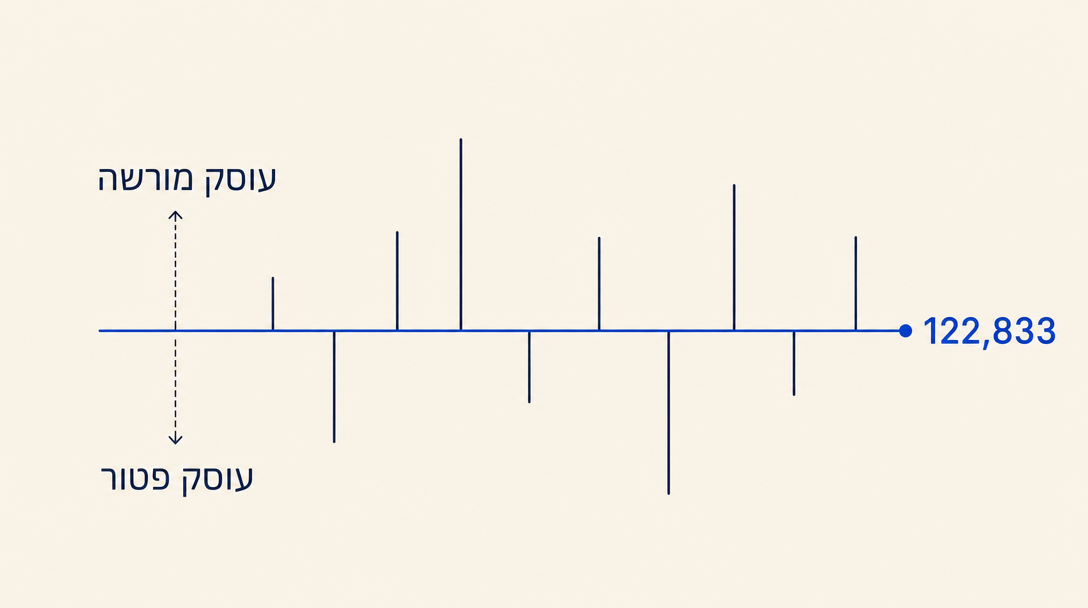

The osek patur vs osek murshe decision

The osek patur threshold in 2026 is ₪122,833 in annual revenue (per Kol Zchut's published threshold). Below it, you can register as an osek patur and skip VAT entirely. Above it, you must be an osek murshe and charge 18% VAT on every invoice.

The threshold is binary, but the decision around it isn't. Ask yourself: what's your forecast revenue for the year?

- Definitively under ₪122,833 (e.g., side income while employed): osek patur.

- Within ±20% of the threshold, not sure either way: see "borderline" below.

- Definitively over ₪122,833: osek murshe.

If you're borderline, the question is: how confident are you that the revenue forecast is right? Because if you're an osek patur and you cross the threshold mid-year, you must convert your file to osek murshe at the Tax Authority within 30 days of crossing, and you become liable for VAT retroactively on any invoices issued at or above the threshold. That retroactive liability is the painful part, you can't go back to clients and bill them VAT for already-paid invoices, so you'd be paying the 18% out of your own pocket on those.

Rule of thumb: if your forecast revenue is within 15% of ₪122,833, start the year as osek murshe. The administrative overhead of monthly Doch Maam is real (an hour or two a month), but it costs you less than the risk of mid-year conversion.

The administrative difference:

| Aspect | Osek patur | Osek murshe |

|---|---|---|

| VAT charged on invoices | None | 18% |

| Doch Maam (VAT return) | None | Monthly or bi-monthly |

| Annual VAT summary | None | January 31 deadline |

| Expense VAT recovery | None | Yes, on business expenses |

| Bookkeeping complexity | Minimal | Moderate (requires invoice-level tracking) |

The "expense VAT recovery" line is what flips some borderline cases. If your business has significant deductible expenses (equipment, software, services from other osek murshe vendors), the 18% you recover on those can offset most of the administrative overhead.

Reading the previous year

Before you decide anything for the current year, read what the previous year is telling you. This is the most overlooked step in the freelancer calendar.

What to look at:

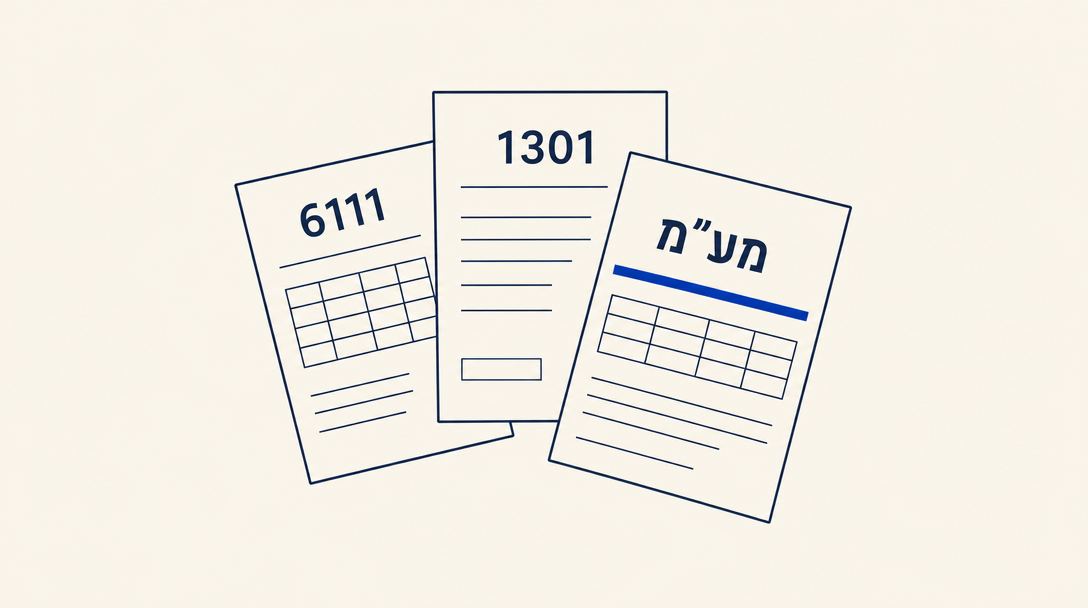

1. Tofes 6111 (financial statement), the annual report your accountant prepared. Specifically look at:

- Revenue trend by quarter. Was Q4 unusually high? Q1 unusually low? That seasonality will repeat.

- Top 5 expense categories. Are they where you expected? Did Section 17 home office come out small because you didn't track it?

- Mkdamot total vs final tax bill. If you significantly over- or under-paid, your mkdamot are set wrong this year and you need a tikun in Q2.

2. Form 1301 from last year, your filed return. Specifically:

- Marginal rate (the bracket your last shekel earned was in). This number tells you the value of every deductible shekel you'll spend this year. At a 35% marginal rate, a ₪1,000 deductible expense saves you ₪350 in tax. At a 24% marginal rate, it saves you ₪240.

- Credits used. Did you claim Section 46 charity? Section 17 home office? Pension contributions? Anything left on the table is your starting list for this year.

3. Doch Maam history, your VAT filings for the year. Look at output VAT vs input VAT by quarter. The ratio tells you whether your invoicing and expense-recovery are seasonally matched.

This 30-minute read of last year's documents is the single highest-ROI activity in the freelancer calendar. It surfaces the strategic decisions you should be making in the current year. Without it, you're just reacting again.

The most common mistake

The mistake most freelancers make is starting the year without reading last year's Tofes 6111. They take last year's mkdamot rate from the Tax Authority's automatic setup, they keep last year's osek patur status without checking the threshold, they don't notice their marginal rate jumped a bracket because Q4 came in 30% over forecast. Then April arrives and they discover a tax bill they could have planned for in Q2.

The fix is mechanical: in mid-January, before any operational decisions, read last year's documents and write down the three numbers (revenue trend, marginal rate, mkdamot vs final). Those three numbers steer everything in this chapter and the next five.

Skills to install for this chapter

israeli-freelancer-ops, set up the deadline alerts for the 12 dates above. Don't try to remember them manually.israeli-bank-connector, pull last year's transactions and categorize them. Useful for the "Tofes 6111 sanity check" if you want to verify what your accountant produced.

If you don't have an accountant and you produced your own Tofes 6111 last year, israeli-tax-returns is the skill that handles the form mechanics. We'll come back to it in chapter 6.

What you should know after this chapter

- The four phases of the year and their distinct postures

- The 12 fixed deadlines and which apply to you

- Whether you should be osek patur or osek murshe this year (with the 2026 ₪122,833 threshold)

- Three numbers from last year that will steer this year's decisions

The next chapter zooms in on VAT cadence, when to file monthly vs bi-monthly, and the one-time decision that determines your administrative load for the year.